Bengalaru, India, June 8, 2026--India's space startup ecosystem has entered its first true execution and commercialization phase, according to the latest assessment by SatNxt. The Indian Space Startup Ecosystem Report 2026 provides a data-led, bottom-up assessment of 230+ active Indian space startups, evaluating technology maturity, execution readiness, capital allocation, business models, and value chain positioning across the full private space sector.

"India's space startup narrative is no longer about who can build compelling technology. In 2026, capital is flowing to those who can execute reliably, survive long development cycles, and scale into global markets," said Aishwary Pachauri, Consultant, SatNxt.

"India's space startup narrative is no longer about who can build compelling technology. In 2026, capital is flowing to those who can execute reliably, survive long development cycles, and scale into global markets," said Aishwary Pachauri, Consultant, SatNxt.

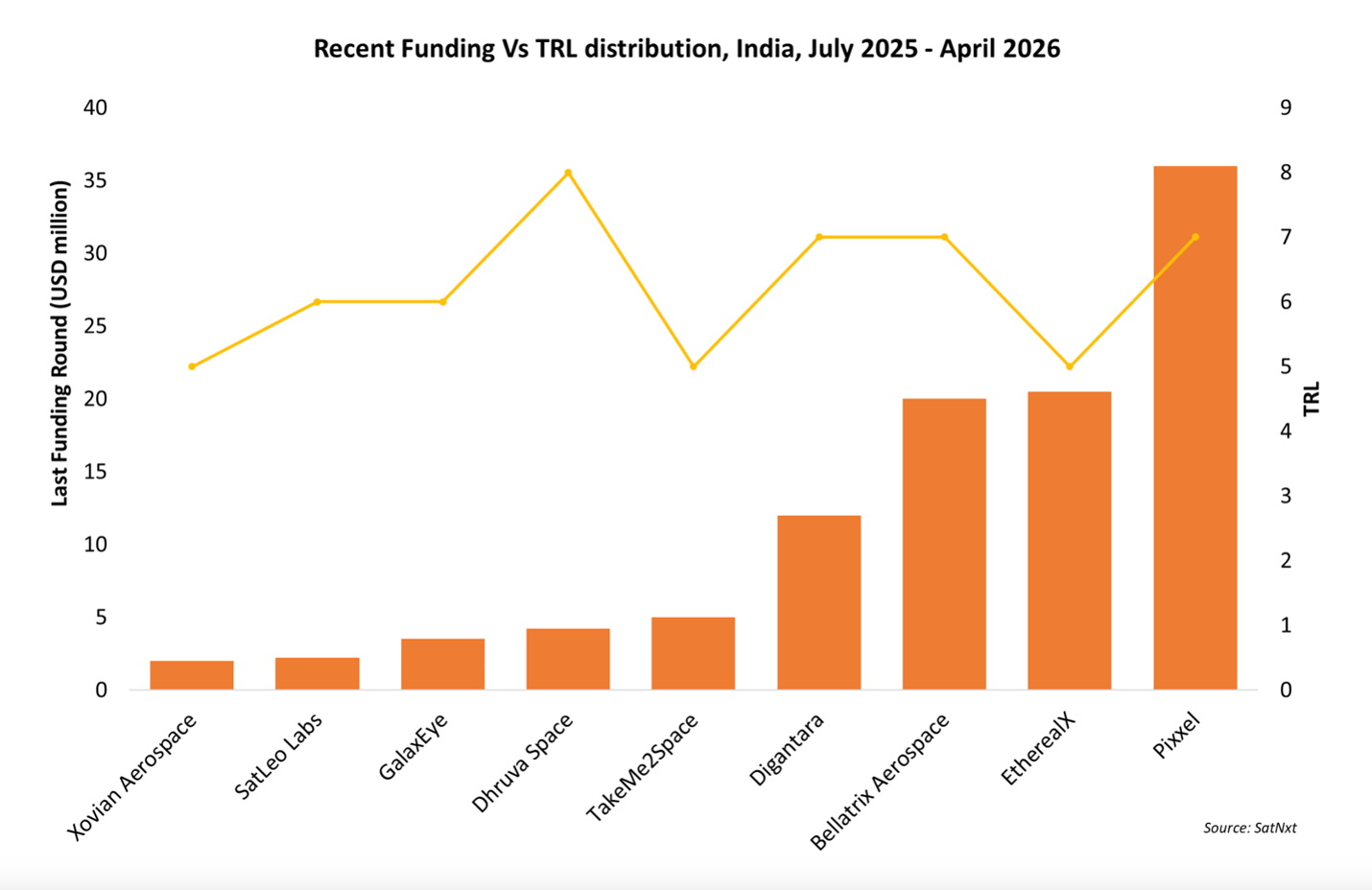

Following the 2020 policy reforms, the market has moved decisively from startup formation momentum to scale, deployment, and revenue realization. Indian space startups attracted over USD 600 million cumulatively between 2020 and 2025. Deal volumes have declined but investor conviction has sharpened, with capital increasingly concentrated at mid-to-high TRLs where execution risk is demonstrably declining. Infrastructure-centric players across launch systems, propulsion, and satellite platforms are drawing the largest rounds, while the mid-TRL financing gap at levels 6 and 7 remains a structural bottleneck.

About the Report

SatNxt's Indian Space Startup Ecosystem Report 2026 is execution-first and evidence-based, built on aggregated company-level data rather than global narratives. The report connects regulatory reform to asset ownership, revenue realization, and capital deployment, offering a consistent framework for assessing readiness and commercial viability across India's private space sector.

What Does the Report Cover?

- How has India's private space sector evolved from an ISRO-centric system to a startup-driven commercial ecosystem?

- Where is capital concentrating across TRL levels, and where does the financing gap persist?

- How are startups classified across business models including hardware, hardware plus service, hardware plus data, and software or data-only models?

- What is the startup activity and capital concentration across Earth Observation, Satellite Communication, and Navigation markets?

- What has been the impact of post-2020 structural reforms and the roles of DoS, ISRO, INSPACe, and NSIL in enabling commercialization?

- Where is sustainable value being created, and where do structural bottlenecks remain?

Key Companies Analyzed

Aadyah Aerospace, AERO2ASTRO, Agnikul Cosmos, Ananth Technologies, Antsys Innovations, Asteria Aerospace, Astrobase, Astrome Technologies, Abyom Space, Bellatrix Aerospace, Blue Sky Analytics, Cosmo Crawler, Cosmicport, Dhruva Space, Digantara, EtherealX, GalaxEye Space, Garuda Aerospace, HEX20 Labs, Hical Technologies, IdeaForge, Infostellar India, InspeCity, KaleidEO, Kawa Space, Kepler Aerospace, Manastu Space, NewSpace Research and Technologies, Omspace Rocket and Exploration, Onnes Cryogenics, PierSight, Pixxel, Saankhya Labs, Sastra Robotics, Satlabs Space Systems, SatSure, Skyroot Aerospace, Space Zone India, Starling Space Technologies, TakeMe2Space, TeamIndus, Tonbo Imaging, VestaSpace Technology, Vyoma Space, XDLINX Space Labs, and 180+ additional companies

Report link: https://www.satnxt.com/reports/indian-space-startup-ecosystem-report-2026