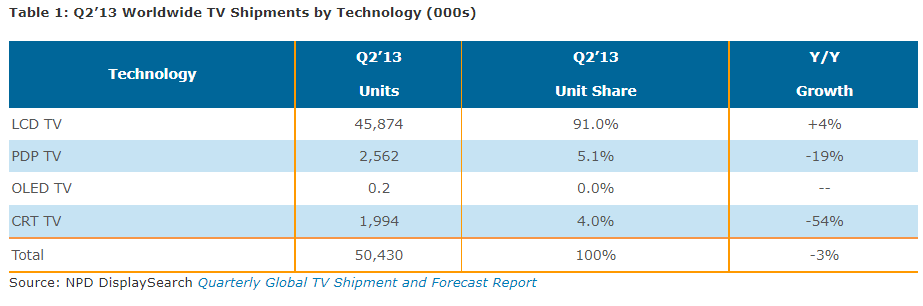

According to the latest findings published in the NPD DisplaySearch Quarterly Global TV Shipment and Forecast Report, Q2‘13 overall worldwide TV shipments were down 3% Y/Y, though LCD TV shipments managed to grow 4% Y/Y. The overall trend in total shipments, while still negative, is showing some improvement from last year, with LCD TV shipments posting slight growth over the past two quarters. China continues to be a catalyst for global LCD TV shipment growth, though Q2’13 growth was likely the result of industry incentives.

“Due to the fact that the government subsidy for energy efficient electronics expired in May, Chinese TV makers shipped a large quantity of LCD TVs in order to take advantage of the subsidy,” said Paul Gagnon, Director of Global TV Research for NPD DisplaySearch.

As a result of the end of the subsidy, China’s LCD TV shipments grew 29% Y/Y in Q2’13, during what is normally a slower seasonal period. Excluding China, global LCD TV shipments fell 3.5% Y/Y, and declined almost 14% Y/Y in developed regions. Western Europe, in particular, experienced a dramatic slowdown in growth, with total TV shipments falling 21% Y/Y, due to poor consumer demand and continued economic headwinds. North America also experienced a sharp drop in TV shipments during Q2’13, with overall units falling 12% Y/Y, as retail inventory pressure suppressed shipments of new models.

Shipments of TVs with the latest new technologies, such as 4K and OLED TV, also started to pick up in Q2’13, although both remained relatively small compared to the TV market as a whole. 4K TV shipments grew to 129K in Q2’13, with the majority of those going to China. At the same time, OLED TV shipments, all from LGE as of Q2’13, increased from 101 in Q1’13 to 208 in Q2’13.

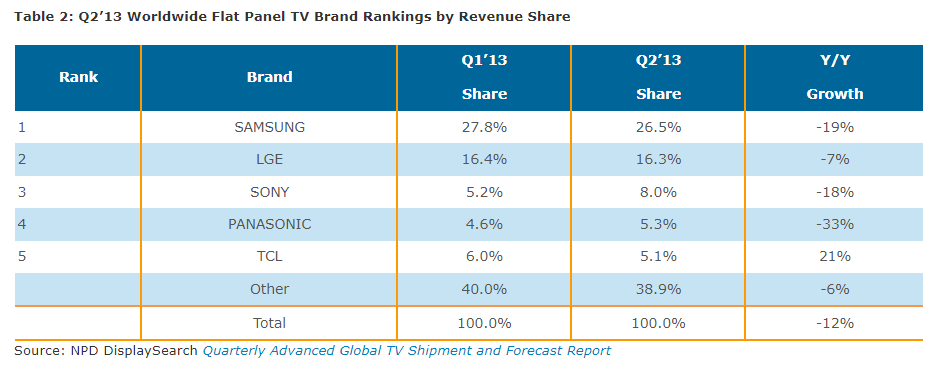

Korean Brands Account for 43% of Global Flat-Panel TV Revenue in Q2’13

Worldwide flat panel TV revenues fell 12% Y/Y in Q2’13. Among the top ten brands, only the Chinese brands grew revenues Y/Y. Samsung remained the leading global flat panel TV brand with more than a 26% share of revenue in Q2’13 (a 1% drop from Q1’13) despite a revenue decline of 19% Y/Y. General market weakness in North America and Europe was a major contributing factor to the decline in revenues, as those two regions account for 45% of Samsung’s global TV revenues.

LG was the second leading brand with almost no change to its flat panel TV revenue share. Sony’s share improved significantly in Q2’13, thanks largely to a growing revenue contribution from China and other emerging markets and strong growth for its average size and share of 4K.

NPD DisplaySearch TV market intelligence, including panel and TV shipments, TV shipments by region/country, brand, size, resolution, frame rate and backlight type for nearly 60 brands, rolling 16-quarter forecasts, TV cost/price forecasts and design wins can be found in the Quarterly Global TV Shipment and Forecast Report. For more information on this report, please contact Charles Camaroto at 1.888.436.7673 or 1.516.625.2452, e-mail contact@displaysear