TV shipments improved 4% Y/Y in Q3’14, and LCD TV shipments alone rose nearly 9%, according to the latest findings in the Quarterly Global TV Shipment and Forecast Report, produced by DisplaySearch, now part of IHS Inc.

Annual TV shipment growth averaged less than 1% on a unit and revenue basis in 1H’14, with LCD TV growth barely compensating for declining shipments of plasma and CRT TVs. However, a continued strong trend of shipment growth in North America continues to be a catalyst, evidenced by LCD TV growth exceeding 12% Y/Y in Q3’14.

LCD TV shipments from China rose 9%, compared to a soft period a year ago following the end of government subsidies, and despite modest sales results during the Chinese Golden Week of public holidays in the fall. Results for the Asia-Pacific region were also quite strong, led by improved growth in an economically stronger India, where more favorable currency valuations are making LCD TVs affordable to a wider group of Indian consumers.

“While the last several years in the TV business have been difficult in terms of overall shipments and revenue, the market is showing some broad resiliency now, with most regions enjoying growth in the third quarter,” said Paul Gagnon, director of global TV research at DisplaySearch. “Consumption for primary TVs is entering a renewed replacement cycle in some key regions, while adoption of larger screens and 4K and other higher resolutions will keep consumers upgrading.”

Although 4K TVs have been available for several years now, shipments in 2014 have significantly accelerated due to broader competition and more accessible price points activating new consumer groups. 4K TV shipments jumped more than 500% Y/Y in Q3’14 to top 3 million units, bringing total shipments to 6.4 million units in 2014.

China remains the focal point for 4K TV unit volume growth, accounting for more than 60% of global 4K TV shipments in Q3; plus, it has the highest share of 4K shipments of any region, at more than 13%. Western Europe is the next strongest region with 6% of 4K TV shipments, a significant increase since the beginning of the year. “With a scarcity of content and streaming options, much of the early success for 4K will rely on education campaigns from brands and price compression that will make it more affordable,” Gagnon said.

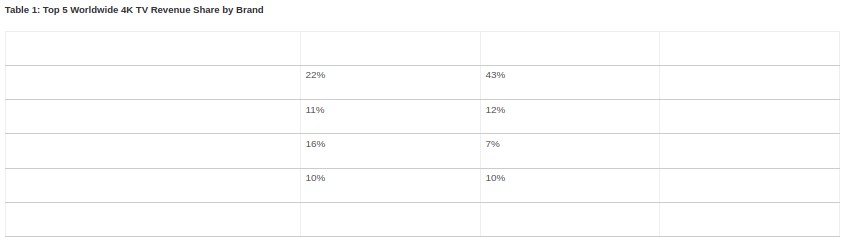

China is the leading 4K TV consumer market, and local Chinese brands are now fiercely competing with Samsung, which is aggressively pushing for growth in China. After debuting a greatly expanded lineup in Q2’14, Samsung leads all 4K brands in the nation. With 36% of the 4K TV shipments, Samsung led the market on a revenue basis globally in Q3’14. The company has significantly outpaced all other brands. Chinese brands have a stronger share thanks to greater volume within China, and a low average price compared to global brands competing in markets outside of China. However, with the arrival of greater competition in North America and other markets, as well as rising 4K TV exports from Chinese brands, competitive price compression will be difficult to avoid for most brands.

Source: DisplaySearch’s Quarterly Advanced Global TV Shipment and Forecast Report

The DisplaySearch Quarterly Advanced Global TV Shipment and Forecast Report includes panel and TV shipments by region and by size for nearly 60 brands. It also includes rolling 16-quarter forecasts, TV cost and price forecasts and design wins. This report is delivered in PowerPoint and includes Excel-based data and tables. If you need further information or assistance please contact us in the United States at 408-418 -1900 or sales@displaysearch.com or at the local DisplaySearch offices in China, Japan, Korea, Taiwan and the United Kingdom.