The latest Ericsson Mobility Report released early this month presents a glimpse of the impressive progress happening in markets on the verge of deploying 5G. It goes beyond the forecast numbers and, in three co-written articles, present a glimpse of the impressive progress happening in markets on the verge of deploying 5G.

With Telstra in Australia, the report explores how to manage the ever-growing demand for data and video, while maintaining consumer experience, particularly for live content streaming. With MTS in Russia, the report describes how mobile networks must evolve to ensure network performance that meets customer experience expectations, as well as enabling new services when preparing for 5G.

And with Turkcell in Turkey, Ericsson looks into managing network performance and service offerings in a successful fixed wireless access (FWA) implementation.

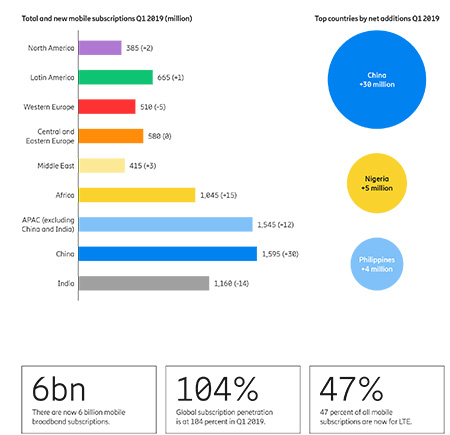

According to the report, the number of mobile subscriptions grew at 2 percent year-on-year and currently totals around 7.9 billion. China had the most net additions during the quarter (+30 million), followed by Nigeria (+5 million) and the Philippines (+4 million). The high subscription growth in China continues from last year, and is likely the result of intense competition among communications service providers in the country. In India, the number of subscriptions declined by 14 million. This was mainly due to the introduction of a minimum regular recharge amount by some large operators, to tackle low-paying users and increase average revenue per user (ARPU).

The number of mobile broadband subscriptions grew at 15 percent year-on-year, increasing by 140 million in Q1 2019. The total is now 6 billion, equalling 76 percent of mobile subscriptions. The number of LTE subscriptions increased by 160 million during the quarter to reach a total of 3.7 billion, and 47 percent of all mobile subscriptions are now for LTE. The net addition for WCDMA/HSPA was around 20 million subscriptions.

The number of mobile broadband subscriptions grew at 15 percent year-on-year, increasing by 140 million in Q1 2019. The total is now 6 billion, equalling 76 percent of mobile subscriptions. The number of LTE subscriptions increased by 160 million during the quarter to reach a total of 3.7 billion, and 47 percent of all mobile subscriptions are now for LTE. The net addition for WCDMA/HSPA was around 20 million subscriptions.

GSM/EDGE-only subscriptions declined by 80 million. Other technologies declined by around 30 million.

Subscriptions associated with smartphones account for more than 60 percent of all mobile phone subscriptions. The number of mobile subscriptions exceeds the population in many countries, which is largely due to inactive subscriptions, multiple device ownership or optimization of subscriptions for different types of calls. As a result, the number of mobile subscribers is lower than the number of mobile subscriptions. Today, there are around 5.7 billion subscribers globally compared to 7.9 billion subscriptions. Global mobile subscription penetration is now at 104 percent.

The report says 5G is on a roll. During the second quarter of 2019 several markets switched on 5G following the introduction of new 5G-compatible smartphones. Some communications service providers have set ambitious targets of reaching up to 90 percent population coverage within the first year. As 5G devices increasingly become available and more service providers launch 5G, over 10 million 5G subscriptions¹ are projected worldwide by the end of 2019.

Looking ahead, in the first five years, 5G subscription uptake is expected to be significantly faster than that of LTE, following its launch back in 2009. On a global level, 5G network deployments are expected to ramp up during 2020, creating the foundation for massive adoption of 5G subscriptions. Most new 5G subscribers will be users trading up their 4G handsets to 5G-compatible devices following 5G services launching in their market. By the end of the period, it is also likely that many young users in mature markets will get a 5G smartphone as their first device.

Given the momentum in the market, Ericsson has increased its forecast for 5G subscriptions, and now expect there to be 1.9 billion 5G subscriptions for enhanced mobile broadband by the end of 2024. This will account for over 20 percent of all mobile subscriptions at that time. The peak of LTE subscriptions is projected for 2022, at around 5.3 billion subscriptions, with the number declining slowly thereafter. However, the report says, LTE will remain the dominant mobile access technology by subscription for the foreseeable future, and it is projected to have nearly 5 billion subscriptions at the end of 2024.

To date, 2G and 3G connectivity has enabled many cellular IoT applications. In recent years, support for large volumes of devices has been enabled by the Massive IoT technologies NB-IoT and Cat-M1 deployed on top of LTE networks.

Cellular IoT use cases will have differing connectivity requirements. A heat sensor in a basement will need deep coverage and have low throughput, whereas a connected robot on a production line may require ultra-low latency, high reliability and high throughput. Cellular IoT use cases can be divided into four segments based on their connectivity requirements.

Massive IoT

This segment primarily includes wide-area use cases, connecting massive numbers of low-complexity, low-cost devices with long battery life and relatively low throughput. Support for these is already being provided in today’s LTE networks with NB-IoT and Cat-M. These technologies complement each other and there is an emerging trend towards service providers deploying one common network supporting both technologies. Cat-M is suited to use cases that require relatively higher throughput, lower latency and voice support, whereas NB-IoT is suited to use cases with very low throughput that are tolerant of delay but require extended coverage.

A copy of the report could be obtained at https://www.ericsson.com/en/mobility-report/reports/june-2019.