Non-geostationary Orbit Constellations Redefining the High Throughput Satellites Market Landscape

Paris, France, April 25, 2024 – Significant and ongoing transformations in the High Throughput Satellites (HTS) market are confirmed in the 7th edition of the 'High Throughput Satellites' report from leading space consulting and market intelligence firm Novaspace, a merger between Euroconsult and SpaceTec Partners. The report underscores the pivotal role of Non-Geostationary Orbit (NGSO) constellations in reshaping the satellite connectivity industry, with the latter to emerge as the primary driver in coming years.

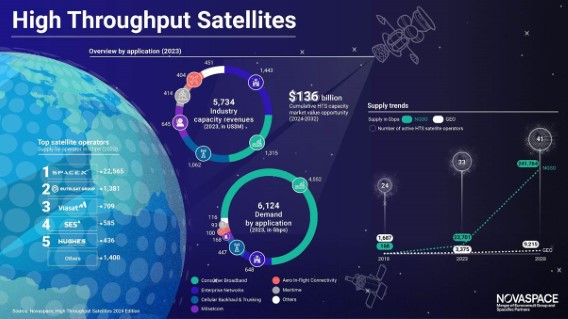

Novaspace’s report reveals that to date, approximately three quarters of the 50+ active satellite operators have invested in HTS systems. The vast majority of HTS players have satellites in GEO orbit. Despite the NGSO potential, high capital expenditure (CapEx) requirements remain a significant barrier for most players, with investments typically between US$ 2-4 billion and exceeding US$ 10 billion for a mega-constellation. As a result, only a select few of the ‘leading’ satellite operators are pursuing plans for full NGSO constellations, with three expected to be operational during 2024. This includes SpaceX’s Starlink, Eutelsat OneWeb and O3b mPOWER from SES.

Recent NGSO dynamism has been mainly supported by the aggressive launch campaign of SpaceX’s Starlink LEO constellation. Overall, HTS supply tripled between 2021 and 2023 to 27 Tbps, with Starlink accounting for 90% of net new supply during the period. The significant increase in supply has been accompanied with strong growth in Starlink’s customer base with the operator reporting >2.7 million customers globally in April 2024.

The emergence of NGSO constellations has forced HTS operators to adapt their strategies. The past few years witnessed an increase in partnerships among satellite operators, with NGSOs featuring in most of them. The rise in NGSO constellations has triggered a wave of ‘multi-orbit’ collaborations among operators, partnering with cross-orbit players in the industry to maximize reach among their customers and to provide them better services across orbits, showcasing the industry's innate adaptability to embrace evolving demands and technologies.

The report forecasts a remarkable nine-fold growth in HTS capacity supply from 2023-2028, with NGSO constellations driving 97% of the net increase. HTS demand doubled in 2023 to 6 Tbps, with NGSO accounting for close to 90% of growth and surpassing GEO in total demand. Consumer broadband, corporate networks and civil government are projected to remain the leading demand drivers.

|

|

HTS capacity demand doubled in 2023; expected to surpass 50 Tbps by 2032. |

Novaspace Managing Consultant Dimitri Buchs commented: “The HTS market is undergoing unprecedented shifts driven by the rapid expansion of NGSO constellations and evolving consumer demands. Interestingly, the influx of subscribers across a variety of verticals for Starlink has led to HTS market expansion, not pure cannibalization, which is a positive indicator for the industry, as it shows that the improved economics enabled by lower HTS capacity pricing should unlock new opportunities both for GEO and NGSO in coming years, as they will allow for better services.”

He added: “The influx of NGSO constellations has not only expanded market supply but has also fostered market competition. This has pushed GEO HTS operators to adapt their strategies and, in response, there has been a limited number of GEO HTS orders in recent years as operators adopt a cautious ‘wait and see’ approach or opt for fully software-defined satellites.”

Small GEO HTS satellites have gained traction in recent years, accounting for half of the eight GEO HTS orders in 2023. Operators favor small satellites due to their lower CapEx requirements, which make financing less challenging and increase the likelihood of recouping investments.

In addition to supply and demand dynamics, the report delves into revenue projections, forecasting a quadrupling of HTS capacity revenue from 2023-2032 to US$ 22 billion in 2032. Despite the dominance of mega-constellations, the report notes that growth remains positive across the market sector. The fastest-growing segments for HTS include land mobility, corporate networks and civil government, with further substantial growth rates expected over the forecast period.